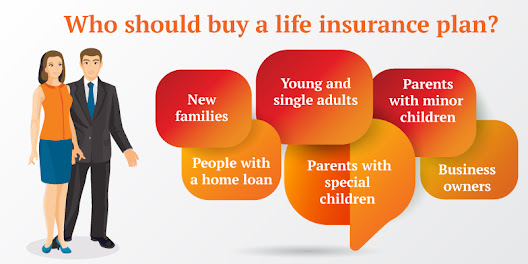

Life Insurance: 9 Tips When Buying for the First Time

It can be hard to imagine a life with a

restricted earning potential. Indeed, everybody understands that life is

unpredictable, and the pandemic has shown us the picture pretty well.

Therefore, it is necessary to ensure your life to protect your loved ones from

uncertainty.

Life insurance will ensure that your loved

ones won’t have to pay the mortgages or loans you have acquired in your

lifetime. Also, having life insurance leaves a legacy for your spouse or

children behind.

But if you’re new to life insurance or

planning to buy a new one, the complexities involved must not discourage you

from applying. Since we understand how challenging it could be for you to

understand everything about insurance, we have compiled a few points to

consider when buying a life insurance policy for the first time.

1. Identify What Plan You Can Afford

Indeed, every individual wants the best plan

for themselves in practice to give a better life to their loved ones. However,

not every plan has the same premium. And therefore, you have to identify what

premium you can afford annually for a life insurance policy.

You can also discuss it with your financial

planner, who can help you assess your life goals and understand what kind of

legacy you want to leave for your spouse or children.

2. Assess the Coverage You Need

It could be challenging for individuals to

identify how much coverage is right for them at times. Generally, people estimate

the coverage relatively less than they actually need. They often miss

calculating the regular monthly expenses like utility bills, children’s

education, etc.

Here’s a hack that can help you with it.

Always have a policy that provides ten times your current annual income as

coverage. Doing so will also help you plan according to inflation for a

specific period.

3. Finding the Right Policy Plan for You

Once you have identified how much you can

afford and what coverage you need, the next important thing is finding the

right policy plan. There are two types of plans available for you to consider,

(i) term insurance and (ii) whole life insurance.

What plan you choose depends on your goals and

finances. However, here’s a distinction between the two that will help you make

a better decision. Term Insurance provides coverage for a certain period, i.e.,

10, 20, or 30 years, and that’s why found to be relatively easy on the

pocket.

Meanwhile, the whole life insurance policy

provides lifelong coverage. That’s why it is costly compared to term life.

Another advantage of having a whole life policy is it adds your cash value. You

can use that cash the way you like, such as using it as an emergency fund,

paying long-term care, or can cover the policy premiums with it.

4. Compare the Different Companies for a Best

Rate

When it comes to buying life insurance, you

must compare different companies to save the best deal. Many companies offer

free quotes on the web, and you can compare them with the ones on top of your

mind.

Besides considering quotes from insurance

companies, you can consult independent insurance agents associated with

different companies to help you suggest the required coverage at the best rate.

You can also consult Alpha Omega Group

Insurance which offers several insurance options such as car insurance, life

insurance, home insurance, etc., at a relatively lesser cost.

5. Consider Your Current and Future Needs

Life insurance is more about tomorrow than

today, and that’s why it is essential to consider your future needs strongly

before purchasing any policy. On the other hand, since life is unpredictable,

ignoring your current needs will also ruin the meaning of having life

insurance. Therefore, you must consider both needs.

Consider your current needs, such as

children’s education or your side business’s expenses. And then see what else

you or your family need money for in the future, such as your child’s college

tuition, retirement savings for your spouse, etc.

6. Consider Critical Illness and Disability

Insurance

Indeed, many people live extraordinary lives

throughout, i.e., free from critical illnesses and disabilities. However, life

is unpredictable and, unfortunately, can show you the days you never want to

face. Your body might develop a disability for any reason, or you might suffer

a critical illness, depriving you of working for a more extended period.

Therefore, combining your life insurance with

critical illness and disability insurance is a good idea. It makes sure that

you don’t have to exhaust your savings when experiencing specific incidents.

Consider at least six to twelve months of

expenses covered in the policy so that your earning power is protected during

tough times.

7. Seek Professional Assistance

You can also contact licensed insurance agents

or professionals associated with different insurance companies; those not only

help you find the right policy but also help you with the budget you have. You

can also have a transparent conversation with the agent with all your doubts

regarding the policy before making the final purchase.

Not even this, by building a relationship with

the insurance agents, you or your family can reach out to them as well when in

need of assistance when making a claim.

8. Prepare to Answer Several Questions When

Applying

Your life insurance premium can vary depending

on your age, health, acute illness, or work you do that exposes you to higher

risk. And that’s when you have to go through a detailed application where you

have to answer all of these questions regarding your mental health, physical

health, and even your and your family’s medical history.

If you are younger, your premium can be lower

as you are less exposed to diseases associated with aging. Besides your age,

questions like tobacco consumption can also be asked during application to

determine your actual insurance rate.

Source Url: https://alphaomegainsurancegroup.com/life-insurance-buying-tips/

Comments

Post a Comment